By Sebastian Manfred Streyffert and Prof. Kristjan Jespersen

Consider a composite example drawn from my thesis interviews. A smaller firm receives sustainability requests from several directions within a short period. A large customer wants emissions figures in its own template. The firm’s bank asks a different set of questions as part of a credit review. A reporting platform requires the same information in a third format. An adviser, brought in to help, recommends a fourth approach. Each request is reasonable on its own. Together, they produce confusion, duplicated effort and a quietly defensive response: do the minimum needed to keep each counterparty satisfied, then move on.

This is not primarily a compliance story. The firm is outside direct CSRD scope and has no statutory obligation to report. The pressure is real, but it arrives sideways, through commercial and financial relationships rather than through law. Once the immediate requests are answered, however, little remains. The firm is often no better equipped to handle the next request than it was before.

That gap – between pressure arriving and capacity forming – is the problem my thesis set out to explain. Across 28 interviews with actors across the Danish ESG reporting ecosystem – SMEs, financial institutions, investors, private equity firms, advisers, industry organisations, reporting platforms and larger companies – the same pattern kept surfacing. ESG-related reporting pressure reaches exposed smaller firms reliably. It just does not reliably stick.

A Simple Way to See Where it Breaks

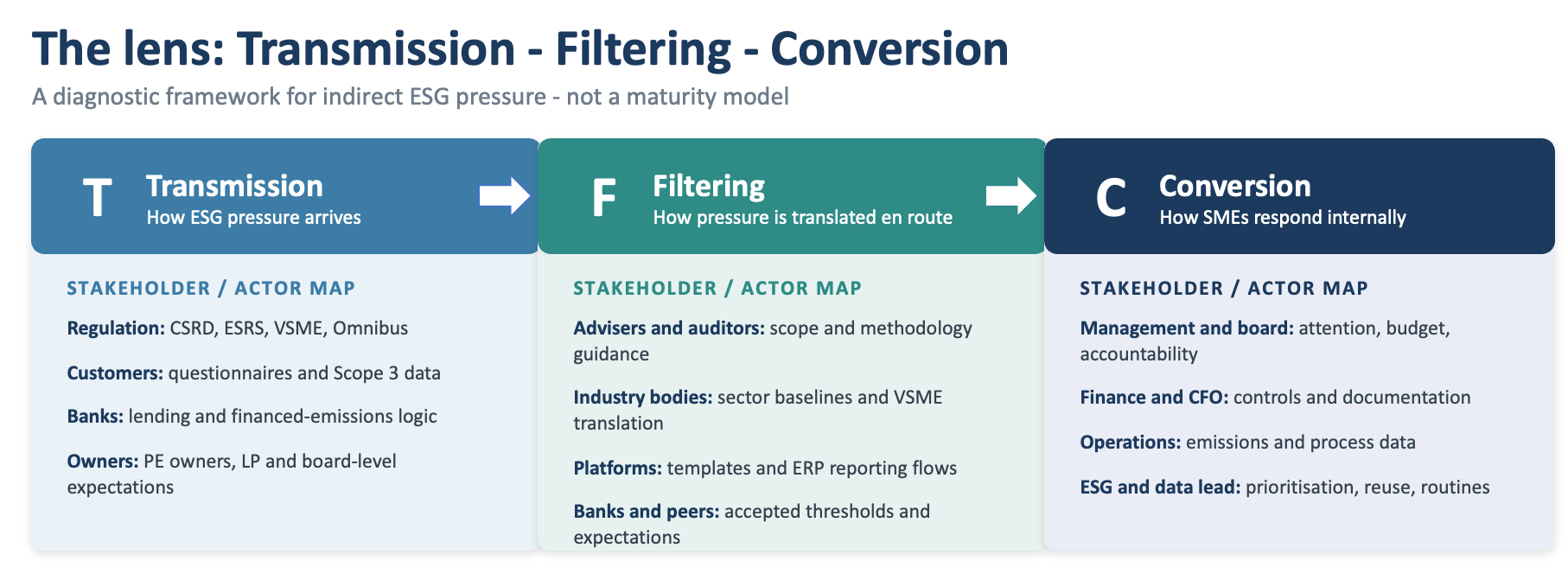

To make sense of this, I use a three-stage diagnostic framework: transmission, filtering and conversion. The point is not the three labels. It is the two hand-offs between them, because that is where pressure tends to leak.

Figure 1. The transmission-filtering-conversion framework explains how external ESG pressure reaches SMEs, is interpreted and is converted – or fails to be converted – into internal capacity.

Transmission is how the pressure travels. For many exposed SMEs, it does not come from regulation directly. It comes through four channels: commercial relationships, where a larger customer needs supplier data to complete its own value-chain reporting; financial actors, where a bank or investor incorporates ESG questions into credit and ownership decisions; ownership structures, where a parent or private equity owner sets expectations from above; and reporting infrastructure, where platforms, templates and questionnaires carry requests that originated elsewhere. A firm can sit outside direct reporting mandates and still be asked for climate data, policies, baselines and reduction plans because someone upstream needs them.

Filtering is how the signal is translated en route and prioritised when it reaches the firm. Advisers, platforms and industry bodies can simplify, standardise, intensify or fragment a request. Management must then decide which requests matter and which are likely to persist. A firm with that clarity can sort the noise. A firm without it treats every request as equally urgent or equally ignorable. When several channels ask differently worded versions of the same question, filtering does not produce one coherent task. It produces several small ones. Transmission was strong; the signal that survived the first hand-off was fragmented.

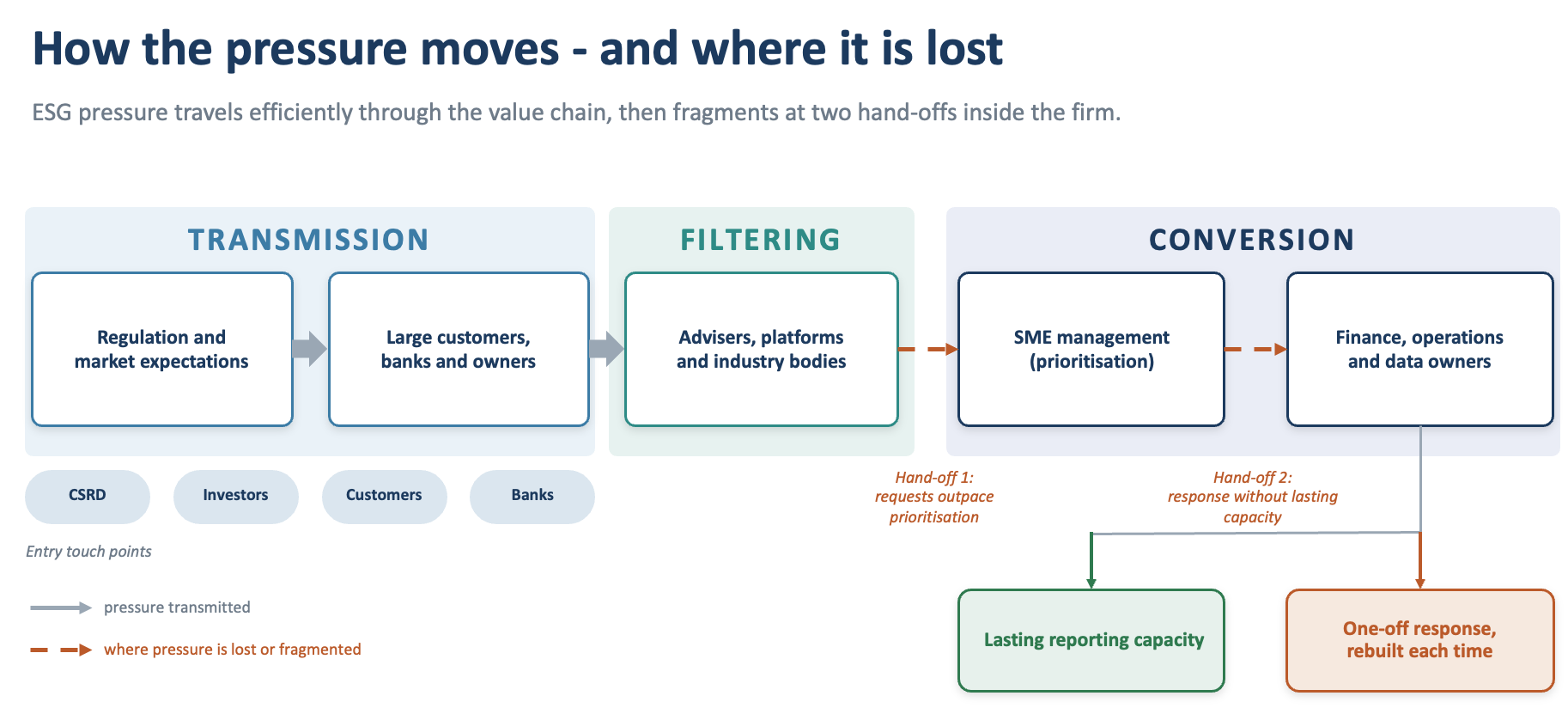

Figure 2. Pressure can move efficiently through the value chain yet fragment at two hand-offs inside the firm: when external requests must be prioritised, and when priorities must become lasting capacity.

Conversion is whether the filtered pressure becomes durable internal capacity – a person, a process or a dataset that can be reused next time. This is the second hand-off, and it is where the deeper failure sits. Responding to a request and building the capacity to respond are not the same thing, and firms routinely do the first without the second.

The Sticking Point

A recurring outcome in my material was neither refusal nor genuine capability. It was what I came to call the minimum-response sticking point. The firm answers enough to satisfy the immediate counterparty, often by assembling figures by hand, then puts the work down until the next request forces it up again. Nothing accumulates. The spreadsheet is rebuilt from scratch each time. ESG sits with whoever has spare capacity that month – finance, operations, sometimes marketing – without a clear mandate or routine behind it.

This is why two firms under broadly similar external pressure can end up in completely different places. Responses ranged from reactive, where the firm does only what the immediate request demands, to strategic, where the firm treats the data as something worth owning. The difference was rarely the strength of the pressure. It was whether the second hand-off – from a filtered request to internal capacity – actually happened. Where it did not, the firm remained reportable on paper while staying unprepared in practice, and the cost of every future request remained high.

Seen this way, the recurring complaint that ‘ESG reporting is a burden for small firms’ becomes more precise. The burden is not simply the existence of requests. It is the repeated, uncoordinated conversion of the same information without the infrastructure or ownership that would let a firm collect it once and reuse it. That is a coordination problem dressed up as a compliance problem. It does not disappear when a firm is taken out of formal scope. If anything, it becomes harder to see because there is no longer a regulation to point at.

Why This Matters Now

The current Omnibus simplification story is that the load on smaller firms has been eased. At the level of direct statutory obligation, that is true. But the transmission channels remain live. Customers still need value-chain data, banks still incorporate ESG into risk dialogue, owners still set expectations and platforms still circulate templates. For exposed SMEs, the pressure has not been switched off. It has been shifted further into the value chain, where firms with limited capacity must filter and convert it.

The useful question, then, is not simply how to add or remove obligations. It is how to make conversion work: how an exposed SME can turn the pressure it receives into capacity it keeps. That depends on conditions outside the firm as much as inside it, and it is the subject I will turn to in a follow-up piece. For now, the diagnosis is enough. The real question is not whether ESG pressure can reach exposed Danish SMEs. It can. The question is whether that pressure becomes lasting reporting capacity – and in many firms, it still does not.

About the Authors

Sebastian Manfred Streyffert recently completed an MSc in Finance and Strategic Management at Copenhagen Business School. His thesis examines how ESG-related reporting pressure reaches exposed Danish SMEs through customers, financial institutions, ownership structures and reporting intermediaries. The study draws on 28 interviews across the Danish ESG reporting ecosystem.

Prof. Kristjan Jespersen is an Associate Professor in Sustainable Innovation and Entrepreneurship at Copenhagen Business School (CBS) and Director of the Nordic ESG Lab. His research focuses on ESG indicators, sustainable finance, and the integration of environmental and climate-related risks into investment decision-making.