By Camilla Solem, Elga Hysa, and Prof. Kristjan Jespersen

Climate change is one of the most significant risks for today’s organizations (TCFD, 2017). Actuaries at the Institute and Faculty of Actuaries (IFoA) now warn that unchecked climate change could wipe out half of global GDP between 2070 and 2090 (Trust et al., 2025; Laville, 2025). For pension funds, whose liabilities stretch decades into the future, those numbers are not distant hypotheticals – they fall squarely within the investment horizon of the savings being set aside today. That makes scientifically grounded climate-risk assessment not merely a technical exercise, but a fiduciary one.

Financial institutions use climate-risk models to assess how their investment portfolios are exposed to climate-related risks. However, recent research has raised concerns that widely used climate-risk models may underestimate the long-term economic consequences of climate change, particularly physical climate risks and the systemic consequences of climate tipping points.

In this post, we examine the climate-risk models used by Danish pension funds and the methodological assumptions behind them. By comparing current modelling practices across providers, we highlight key limitations in existing models and discuss how pension funds can strengthen their climate-risk assessments.

How Climate-Risk Models Work

Climate-risk models aim to estimate the financial impact of climate change on economic activity, asset values, and investment portfolios. These models can be built around different assumptions and rely on two foundational components: climate scenarios and damage functions.

Climate scenarios enable organizations to better understand and test the resilience of their strategies and portfolio under different potential climate futures. Scenario frameworks developed by institutions such as the Intergovernmental Panel on Climate Change (IPCC) and the Network for Greening the Financial System (NGFS) are widely used in the financial sector. However, it’s important to note that they represent hypothetical pathways and are not designed to give precise predictions of the future or quantify the financial implications of these futures.

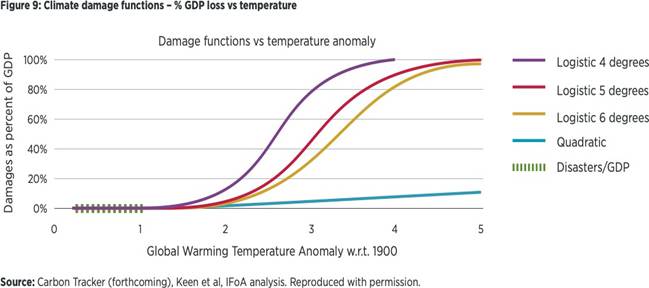

Climate-risk models fill this gap by translating scenario outcomes into economic impacts. This is possible through the presence of a damage function, which quantifies the relationship between global temperature change and economic loss. Two of the most commonly used damage functions in climate-risk models are quadratic and logistic. The quadratic damage function assumes a smooth and gradual increase in GDP losses as temperature rises. As it excludes tipping points and abrupt system changes, it produces relatively low estimates of GDP losses even at high levels of warming (like 5°C). By contrast, the logistic damage function assumes that economies can adapt only up to a certain point, after which losses accelerate rapidly and may approach total collapse.

Source: Trust et al. (2023), p. 25

Finally, models can also differ based on their level of analysis. Bottom-up models assess climate risks at the company or asset level and aggregate these impacts across a portfolio, while top-down models estimate macroeconomic effects (GDP, productivity) first and then translate these shocks to asset classes or portfolios.

All these methodological choices strongly influence model outcomes and can lead to significantly different estimates of climate-related financial risks.

Climate-Risk Models Used by Danish Pension Funds

The findings from the analysis show that Danish pension funds rely heavily on externally developed climate-risk models, with MSCI’s Climate Value-at-Risk (CVaR) model being the most widely used framework for assessing climate risk. Most pension funds that use this model apply climate scenarios developed by the NGFS, typically assessing portfolio exposure under scenarios corresponding to approximately 1.5°C, 2°C and 3°C of global warming. This model captures both transition risks, such as policy changes and technological shifts, and physical risks, referring to direct or physical damage to assets caused by events such as floods or rising temperatures.

Despite the growing use of these models, the findings reveal considerable uncertainty among pension funds regarding the reliability of current modelling approaches. There were concerns that existing models may underestimate physical climate risks, particularly over long-term time horizons. This was evident as certain model outputs suggested that higher temperature scenarios could result in relatively limited negative impacts on portfolios – an intuitively surprising result that several funds themselves flagged.

Limitations in Current Climate-Risk Models

When using climate-risk models it is important to be aware of their potential limitations. First, there are concerns that existing models may underestimate climate-related risks. Earlier versions of MSCI’s CVaR model relied primarily on a bottom-up approach focused on company-level exposure. This approach made it difficult to capture broader systemic impacts of climate change on the global economy. For instance, Norges Bank Investment Management (NBIM) estimated significantly larger economic losses in its internal top-down model than those produced by the earlier CVaR framework. Recent updates to the MSCI CVaR methodology have attempted to address this limitation by using updated NGFS Phase V scenarios and introducing a macroeconomic physical risk component and adding an additional layer to the damage functions to capture the nonlinear, accelerating economic losses related to physical impacts.

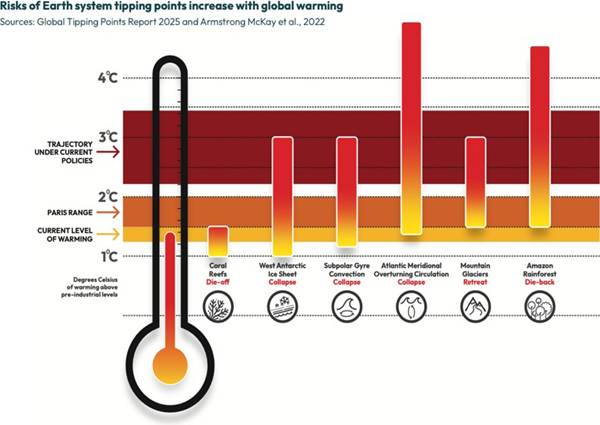

Another limitation of current models is the exclusion of explicit modelling of climate tipping points. Climate science increasingly highlights the risk that relatively small increases in global temperature may trigger abrupt and potentially irreversible changes in the Earth system. Because most climate-risk models do not explicitly incorporate these tipping points, they may underestimate the potential magnitude of long-term physical and systemic risks.

Source: Lenton et al. (2025)

Another important methodological element to be aware of with the MSCI CVaR model is that it discounts future climate-related costs and damages to present value to estimate their impact on current company valuations. While this approach is common in financial modelling, it means that climate risks occurring further in the future appear less significant in today’s valuation calculations. For long-term investors such as pension funds, this discounting mechanism may downplay risks that are highly relevant over their investment horizon.

Alternative Modelling Approaches

There are alternative modelling approaches that attempt to address some of these limitations. One example is Ortec Finance’s ClimateMAPS framework, a climate-scenario tool designed specifically for long-term institutional investors. ClimateMAPS uses top-down economic modelling combined with nonlinear damage functions and explicitly incorporates selected climate tipping points. These modelling choices lead to more pessimistic projections of long-term economic impacts compared to models based on NGFS scenarios alone.

Source: Ortec Finance (n.d.)

Another key difference from the MSCI CVaR model is that ClimateMAPS can be integrated into Ortec’s GLASS framework, which provides year-by-year economic evolution without collapsing everything into a single discounted number.

Conclusion

Climate-risk modelling is becoming an essential tool for institutional investors seeking to understand the financial implications of climate change. Danish pension funds have begun integrating such models into their investment processes, but the analysis shows that important methodological limitations remain, and confidence in current model outputs is still constrained.

In particular, the exclusion of climate tipping points and the discounting of long-term impacts may lead to an underestimation of physical climate risks. These individual model limitations risk turning into systemic blind spots when there is an overreliance on a single vendor. As climate-risk modelling evolves, actors must develop stronger internal expertise and critically assess the models they use to ensure climate risks are reflected in long-term investment decisions.

For Danish pension funds, the question is no longer whether to use climate-risk models, and whether they already do, but whether those models can carry the weight being placed on them. Building internal expertise, diversifying modelling approaches, and interrogating the assumptions embedded in external vendors are no longer optional; they are prerequisites for managing a risk that current frameworks may be systematically under-pricing.

References

Laville, S. (2025, January 16). Global economy could face 50% loss in GDP between 2070 and 2090 from climate shocks, say actuaries. The Guardian. https://www.theguardian.com/environment/2025/jan/16/economic-growth-could-fall-50-over-20-years-from-climate-shocks-say-actuaries

Lenton, T. M., Milkoreit, M., Willcock, S., Abrams, J. F., Armstrong McKay, D. I., Buxton, J. E., Donges, J. F., Loriani, S., Wunderling, N., Alkemade, F., Barrett, M., Constantino, S., Powell, T., Smith, S. R., Boulton, C. A., Pinho, P., Dijkstra, H. A., Pearce-Kelly, P., Roman-Cuesta, R. M., Dennis, D. (eds). (2025). The Global Tipping Points Report 2025. University of Exeter, Exeter, UK. https://global-tipping-points.org/

Ortec Finance. (n.d.). The role of damage functions in assessing physical climate risks. https://www.ortecfinance.com/en/insights/blog/the-role-of-damage-functions-in-assessing-physical-climate-risks

Task Force on Climate-Related Financial Disclosures (TCFD). (2017, June). Final Report: Recommendations of the Task Force on Climate-Related Financial Disclosures. https://assets.bbhub.io/company/sites/60/2021/10/FINAL-2017-TCFD-Report.pdf

Trust, S., Saye, L., Bettis, O., Bedenham, G., Hampshire, O., Lenton, T. M., & Abrams, J. F. (2025, January 16). Planetary Solvency — Finding our balance with nature. Global Tipping Points. https://global-tipping-points.org/wp-content/uploads/2025/09/planetary-solvency-finding-our-balance-with-nature.pdf

Trust, S., Joshi, S., Lenton, T., & Oliver, J. (2023, July). The Emperor’s New Climate Scenarios. British Institute and Faculty of Actuaries. https://actuaries.org.uk/media/qeydewmk/the-emperor-s-new-climate-scenarios.pdf

About the Authors

Camilla Kjellevold Solem is completing her MSc in Strategy, Organization and Leadership at Copenhagen Business School, with a minor in ESG: Metrics, Reporting and Sustainable Investments. Her master’s thesis investigates how Norwegian companies make sense of the EU Omnibus I simplification package and what this means for the future of corporate sustainability work. Alongside her studies, she has worked as a Customer Experience Specialist at Penneo. What drives her is a fundamental curiosity about how organizations truly embed sustainability, and how to effectively lead this change.

Elga Hysa is completing her MSc in Strategy, Organization and Leadership at Copenhagen Business School, with a minor in ESG: Metrics, Reporting and Sustainable Investments. Alongside her studies, she works at DSV in Group Operational Sustainability, where she contributes to the cross-divisional and cross-regional alignment of the company’s sustainability strategy and supports its ongoing improvement. What drives her is understanding the intersection of corporate and sustainability strategy, particularly how long-term environmental and organizational goals translate into short-term decision-making within complex global organizations.

Prof. Kristjan Jespersen is an Associate Professor in Sustainable Innovation and Entrepreneurship at Copenhagen Business School (CBS) and Director of the Nordic ESG Lab. His research focuses on ESG indicators, sustainable finance, and the integration of environmental and climate-related risks into investment decision-making.