By Silje Thon Skaanes, Freja Hejlskov, Kristine Aass Rud and Prof. Kristjan Jespersen

Key Takeaways: Current ESG ratings reward disclosure maturity over genuine inclusion outcomes. A new DEI Performance Model (DPM) tested on 9,000+ companies across 95 countries quantifies both representation and belonging – and penalises imbalance between the two. For investors, the DPM offers a more credible tool for portfolio screening and targeted engagement

For years, the debate around diversity, equity, and inclusion (DEI) in corporate settings has run into the same problem: what gets measured gets managed, yet what is being measured is often the wrong thing. DEI has moved firmly into the mainstream of corporate governance, sustainability reporting, and investor due diligence. And yet a credible, holistic, and investment-grade measure of DEI performance remains elusive. This blog post introduces new research from Copenhagen Business School that proposes a structured framework – the DEI Performance Model (DPM) – to address this gap.

The dominant assumption in many organisations is that workplaces operate as pure meritocracies, where talent alone determines advancement. The evidence consistently contradicts this view. Modern discrimination rarely manifests at the hiring gate alone; it operates through the cumulative accumulation of everyday micro-processes which subjective managerial judgements, opaque promotion criteria, and unequal perceptions of comparable contributions (Pager & Shepherd, 2008). These invisible disadvantages compound over time, systematically disadvantaging minority employees, whose performance ratings are demonstrably more susceptible to stereotype-based evaluation bias (Pulakos et al., 2019; Elvira & Town, 2001). If capital markets are expected to reward talent allocation efficiently, then the capacity to measure whether organisations actually create equal opportunities is not merely an ethical imperative but also financial one.

The DEI Data Problem Is Worse Than You Think

The core challenge is not simply data scarcity. The data that do exist are fragmented, methodologically inconsistent, and susceptible to misinterpretation (Kotsantonis & Serafeim, 2019). A structural bias towards input-based indicators compounds the problem: OECD analysis suggests that output-based metrics account for only around one-third of standard ESG measures, with the remainder comprising policy proxies and management disclosures that infer performance rather than directly measuring it (OECD, 2025).

Input-based metrics cannot capture the systemic conditions that produce, reproduce, or mitigate discrimination within organisations. More critically, they measure representation indicators in isolation, detached from the organisational dynamics that determine whether diverse employees actually experience inclusion or equitable outcomes (Luthra & Muhr, 2023). A company can achieve a high diversity score by hiring proportionally across demographic groups, while its culture quietly excludes those same employees from informal networks, sponsorship, and promotion. Current ESG ratings, by rewarding disclosure maturity over outcome quality, risk encoding this gap into investor decision-making (Bowe et al., 2023; Huber et al., 2023).

“ESG scores increasingly reward disclosure maturity rather than capturing whether diverse employees truly experience inclusion or equitable outcomes.” – a structural limitation that distorts market signals and undermines the business case for genuine inclusion.

Introducing the DEI Performance Model: No Diversity without Inclusion

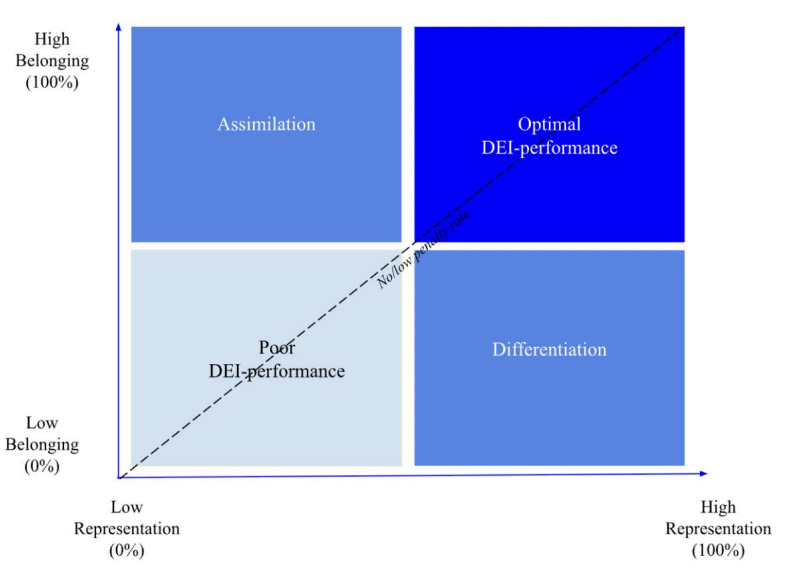

To address this structural gap, the research proposes the DEI Performance Model (DPM): a two-pillar framework that translates fragmented and often incomparable ESG data into an interpretable, actionable assessment of DEI performance. The model is grounded in Optimal Distinctiveness Theory (ODT), which posits that individuals hold two simultaneous, and potentially conflicting, needs: to feel validated as part of a group, and to retain a sense of unique identity (Brewer, 1991; Shore et al., 2011; Luthra & Muhr, 2023).

Genuine inclusion, in this framework, is not achieved by maximising either assimilation or differentiation. It is achieved when both needs are met in balance. Too much enforced similarity generates resentment and internal competition; too much isolation reinforces exclusion and stereotype threat (Shore et al., 2011). The DPM operationalises this insight into a measurable structure.

Figure 1: The Balance between Representation & Belonging based on the ODT (inspired by Luthra & Muhr, 2023).

The Architecture of the Diversity Performance Model

The Representation Pillar reflects “who gets in” and “who progresses” in an organization, which can highlight possible biases and glass ceilings that might exist (Taparia & Lenka, 2022). The Belonging Pillar captures whether under-represented groups feel included:

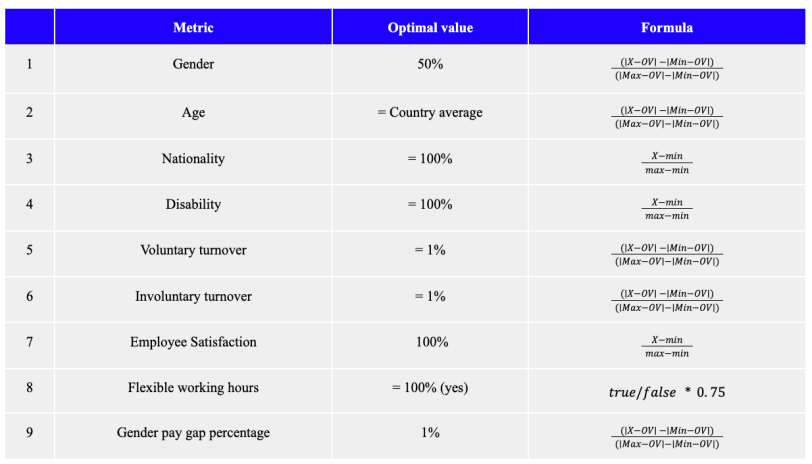

Table 1: Included metrics in the DPM

How the Model Calculates

The model calculates as:

DEI Performance = 0.5 × Representation + 0.5 × Belonging − Penalty

In order to ensure comparability across metrics and companies, each metric is normalised. For metrics where 100% is optimal, we use standard min-max normalization: (X−min)/(max−min). For metrics where 100% is not the optimal value, a parity is calculated: Parity = |X − OV|, where X refers to the company score and OV refers to the optimal score. This ensures that higher raw values translate into lower normalised scores when they indicate worse performance. For example, gender distribution has an optimal value of 50%, where the best score is closest to 50% (regardless of whether the reported number is above or below 50%), and the worst score is furthest from 50%.

The Representation pillar aggregates scores across Workforce, Leadership, and Board levels, with each level averaging its four sub-metrics. The Belonging pillar averages its five metrics, with flexible working hours weighted at 0.75 to avoid overweighting a binary indicator. These two pillars together refer to the DEI base.

The penalty mechanism is critical: Penalty = DEI base × Imbalance, where imbalance is the absolute difference between Representation and Belonging scores. In line with the ODT and the DPM, high representation scores have no true value if not accompanied by equally high inclusion rates and vice versa. This calculation ensures a penalty that increases proportionally with the size of the imbalance, preventing organizations from achieving high scores through representation alone without fostering genuine inclusion.

What This Means for Investors

The DPM offers investors several practical applications. As a portfolio screening tool, it enables more credible differentiation among companies on the social dimension of ESG than existing ratings which, as noted, often conflate disclosure quality with performance quality. As an engagement tool, it provides a structured basis for targeted dialogue with portfolio companies: identifying whether underperformance is driven by weak representation, inadequate belonging infrastructure, or the imbalance between the two has direct implications for the nature of engagement.

From a fiduciary perspective, the model’s capacity to surface hidden risks is material. A company with strong diversity optics but poor belonging scores may face elevated exposure to retention risk, legal liability, and reputational damage/risks that do not appear in conventional DEI metrics but are captured in the DPM’s penalty logic.

For investors, the DPM reframes DEI from a compliance exercise into a risk and opportunity lens – one that is rigorous enough to support allocation decisions and engagement strategies alike.

Several limitations and development priorities are worth flagging. The model currently applies a universal scoring logic that does not fully account for structural and cultural heterogeneity across regions and industries. Future enhancements – including industry-specific and country-specific weightings, and a more granular penalty calibration – would materially improve the model’s contextual sensitivity. Data availability also remains a constraint; the model’s scope is bounded by what companies disclose, which itself reflects the current state of the reporting ecosystem rather than the full range of relevant DEI dynamics.

Conclusion: Measuring the Unmeasured

The growing institutionalisation of DEI within investment frameworks is a welcome development. But it will only deliver its promised impact if the metrics underpinning those frameworks actually measure what they purport to measure. The current generation of DEI indicators largely does not. The DEI Performance Model presented here represents a step towards closing that gap by measuring representation and belonging jointly, penalising their imbalance, and grounding the methodology in a theoretically coherent framework.

True meritocracy cannot exist when systemic barriers remain invisible and unmeasured. The DPM is an attempt to make them visible and to give investors, companies, and researchers the tools to act on what they find.

About the Authors

Silje Thon Skaanes is currently completing her MSc in Business and Development Studies at Copenhagen Business School, with a minor in ESG and a specialisation in the Spanish language, complemented by a year studying Spanish language and politics at the University of Barcelona. With professional and academic experience spanning the RoPax, cruise, LNG, and port sector, she has developed a strong interest at the intersection of the maritime industry and climate-related risk management. Her bachelor’s thesis explored shipping decarbonisation, and her master’s thesis investigates the mechanisms through which a green value proposition can be achieved in the container port industry, using a fully electrified and partly automated APM Terminal in Croatia as a case study. Alongside her studies, Silje works as a Digital Marketing Student Assistant in the MarCom department at Go Nordic Cruiseline. The role of context and culture in sustainable development is of particular interest to her, especially within emerging economies and developing countries.

Freja Hejlskov is finalising her MSc in Diversity & Change Management at Copenhagen Business School, where she has also pursued a minor in ESG. Her master’s thesis explores how Spanish mining companies navigate the trade-offs between CRMA requirements, economic objectives, and minimizing environmental and social impact, addressing the broader paradox of enabling a green transition through resource extraction. Next to her studies, she works as a People & Culture Assistant at PSV, a venture house, where she has focused on DEI within startups and investment processes, with a particular emphasis on advancing gender diversity in the tech-investments. Her passion for people, social sustainability and DEI has been a consistent thread throughout her academic and professional journey, including her bachelor’s thesis on DEI in SMEs and her experience working at FLA Leadership.

Kristine Aass Rud is currently completing her MSc in Business and Development Studies at Copenhagen Business School, with a minor in ESG. She has developed a strong regional focus on Spanish-speaking markets, building on her academic and international experience, including an exchange semester at Tecnológico de Monterrey in Mexico City during her bachelor’s degree. Her master’s thesis explores energy justice in Peru, a topic she has engaged with firsthand through recent fieldwork in Cusco. Alongside her studies, Kristine is actively involved in her program’s student union and works at a global logistics company, gaining practical experience in an international business environment. She is particularly driven by issues related to ESG, the green energy transition, and the development of emerging markets.

Prof. Kristjan Jespersen is an Associate Professor in Sustainable Innovation and Entrepreneurship at the Copenhagen Business School (CBS). Kristjan is an Associate Professor at the Copenhagen Business School (CBS). As a primary area of focus, he studies the growing development and management of Ecosystem Services in developing countries. Within the field, Kristjan focuses his attention on the institutional legitimacy of such initiatives and the overall compensation tools used to ensure compliance. He has a background in International Relations and Economics.