By Daniel Schou, Nelly Chi, Sebastian Manfred Streyffert, and Christian Munch Jørgensen and Prof. Kristjan Jespersen

The Translation Gap

There is a persistent and costly blind spot at the heart of private market investing: climate and nature risks rarely get translated into the financial variables that drive investment decisions. On the public markets side, a portfolio manager can pull data like Climate Value at Risk from MSCI and, quite easily, size up exposure at the asset and portfolio level. In private markets, the gap is wider than most assume. The usual suspect is data scarcity, but that is only half the story. The deeper problem is the absence of a structured bridge from risk signals to valuation. In practice, climate and nature risks are too often buried under broad ‘ESG risk’ labels, assessed through qualitative heatmaps, inconsistent terminology, and checkbox exercises. Treating these as “soft topics” erodes risk comparability across assets, funds, and managers, and strips information of its utility for pricing, insurance, portfolio steering, and reporting. That is a costly mistake, because what is not understood cannot be managed, and what cannot be managed is unpriced exposure sitting quietly on the balance sheet.

The stakes are not abstract. Climate and nature risks span both physical and transition categorizations established by TCFD (2017) and TNFD (2023), and the urgency is accelerating alongside our understanding of the underlying science. Global insured losses from natural catastrophes hit $137 billion in 2024, growing 5 to 7% annually in real terms (Swiss Re, 2025), while Bloomberg (2026) finds that 10pp higher physical asset damage risk corresponds to 22bp higher cost of capital. Nature risk is no less material, with losses already estimated at $430 billion annually across eight major sectors (Ceres, 2025). Yet the practices of managers in private markets still do not reflect this financial materiality. Figures from PRI (2025) show that only 22% of private equity managers disclose physical climate risk metrics, and just 29% of infrastructure investors report them publicly. Unwritten’s 2025 analysis of 70 private market reports exposes a parallel failure in ongoing monitoring: 67% of firms incorporate climate risk in pre investment due diligence, but only 13% extend that monitoring through the full asset lifecycle.

The market is moving fast, and the bar is rising. NBIM, through its 2030 Climate Action Plan published in October 2025, commits to quantify all physical climate risk at the asset level across its unlisted real assets, to integrate climate and nature risks directly in its portfolio adjustments, and to deploy AI driven analytics on proprietary data. When allocators of that scale operationalize such detailed risk assessment, they signal precisely where the market is heading and what will be expected of every manager they allocate to. For the manager that still governs climate and nature risk softly, we therefore ask you: what happens when your largest LP can price the risk in your portfolio more precisely than you can?

Two things are missing in current practice: first, the quantification of climate and nature risks in financial terms; and second, a shared understanding of those risks across investment functions. The framework proposed here addresses both, with a clear ambition: climate and nature risks should be treated like any other financial risk exposure, not siloed as an “ESG” concern, but owned by the same people and subject to the same scrutiny.

Proposition: A Risk Taxonomy for Translating Climate and Nature Value at Stake

Premise and Assumptions

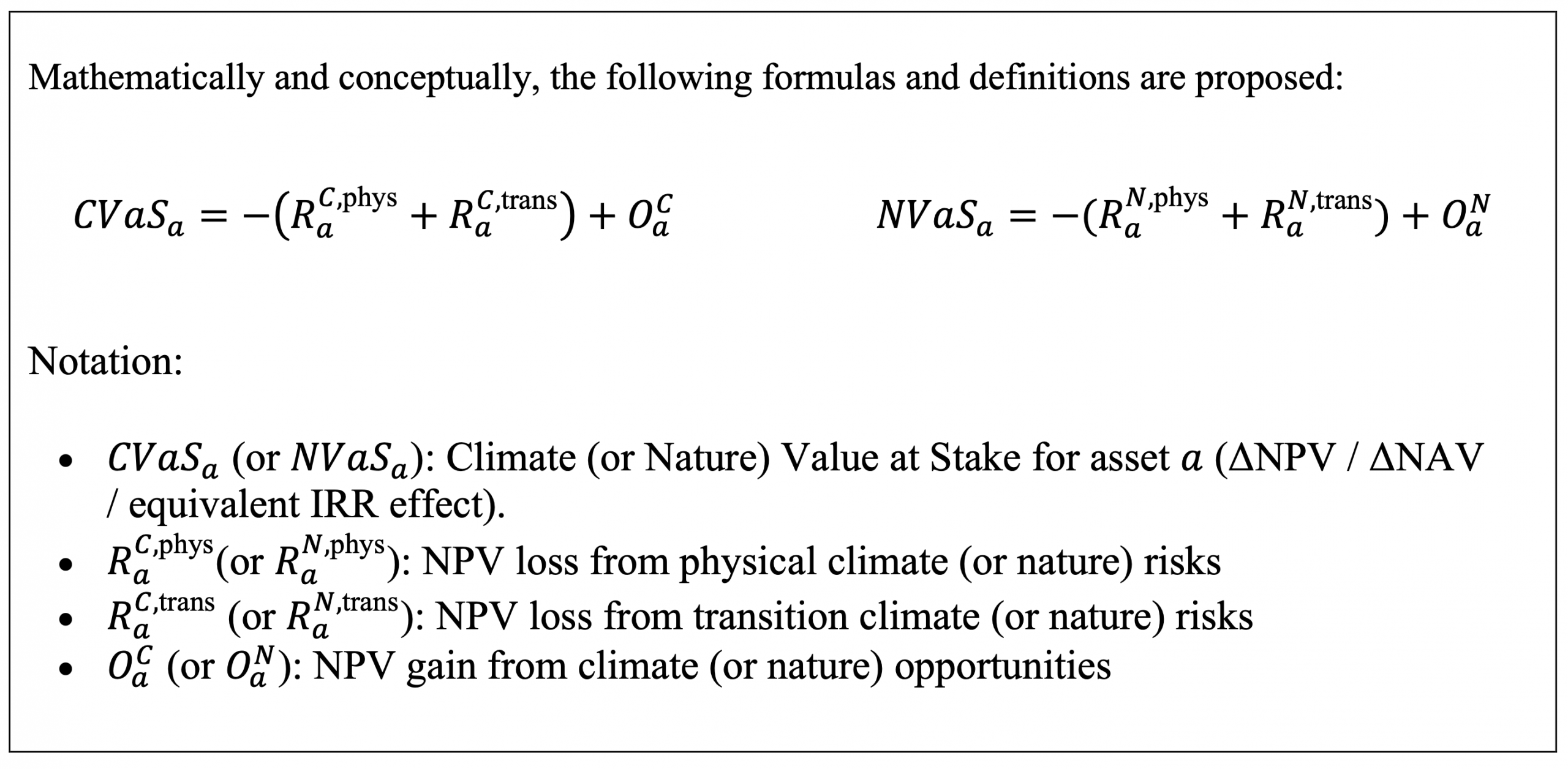

The proposition is conceptually elegant: climate and nature exposures are treated as value adjustments to an existing baseline, expressed as “Value at Stake” (VaS). The framework assumes that each asset carries a base case valuation metric (NPV/NAV/IRR) without explicit climate or nature adjustments, and that both risks and opportunities can be monetized as changes to that baseline. Risks reduce present value; opportunities add to it. Once VaS is expressed at the asset level, figures aggregate upward to the fund and manager level using economic exposure weights such as NAV or invested capital shares. Drawing inspiration from statistical VaR percentiles used in market risk, VaS is best understood as the expected effect of applied assumptions across specific climate and nature scenarios.

Proposed Framework and Core Methodology

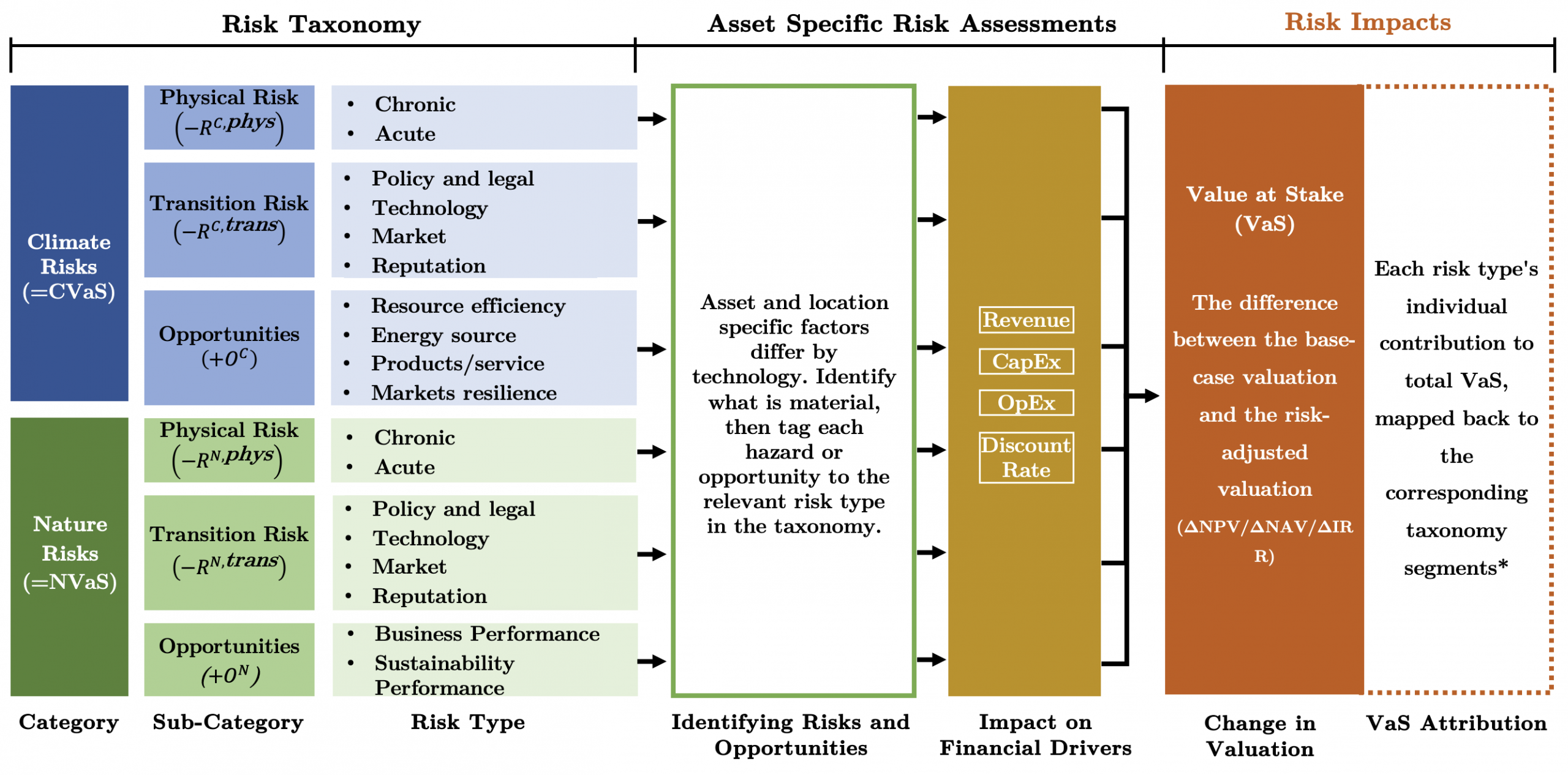

The taxonomy is structured in three layers: Category, Sub category, and Risk type, all anchored in TCFD (2017) and TNFD (2023) terminology. At the highest level, it distinguishes between Climate Risks and Nature Risks, each divided into physical risks, transition risks, and opportunities, with explicit risk types beneath each. The full structure is illustrated in Figure 1.

Figure 1: Risk Taxonomy for Climate and Nature Risk. Source: Authors’ own conceptual model based on TCFD (2017) and TNFD (2023).*Attribution of total VaS to Risk Taxonomy segments should follow a standalone sensitivity approach with proportional allocation of interaction effects.

Asset level Climate Value at Stake (CVaS) and Nature Value at Stake (NVaS) treat climate and nature as explicit value adjustments to an existing base case valuation, expressed in changes in NPV, NAV, or IRR terms. In practice, assessments begin at the asset level. Risk signals relevant to each asset’s technology and location are translated into expected financial effects through existing budget items: revenue, OpEx, CapEx, and the Discount Rate. Each asset is assumed to have a baseline valuation without climate or nature considerations, with CVaS and NVaS representing the monetised change to that baseline driven by risks and opportunities. CVaS reflects the combined effect of physical and transition climate risks alongside climate related opportunities, while NVaS reflects the effect of physical and transition nature risks that reduce value and nature related opportunities that increase value. In both cases, value impacts are decomposed into three blocks: physical risks, transition risks, and opportunities. Physical risks are divided into acute and chronic components, while transition risks are structured across policy and legal, technology, market, and reputation channels. Climate opportunities follow established categories such as resource efficiency, energy sources, products and services, and market resilience, while nature opportunities are structured around business performance and sustainability performance.

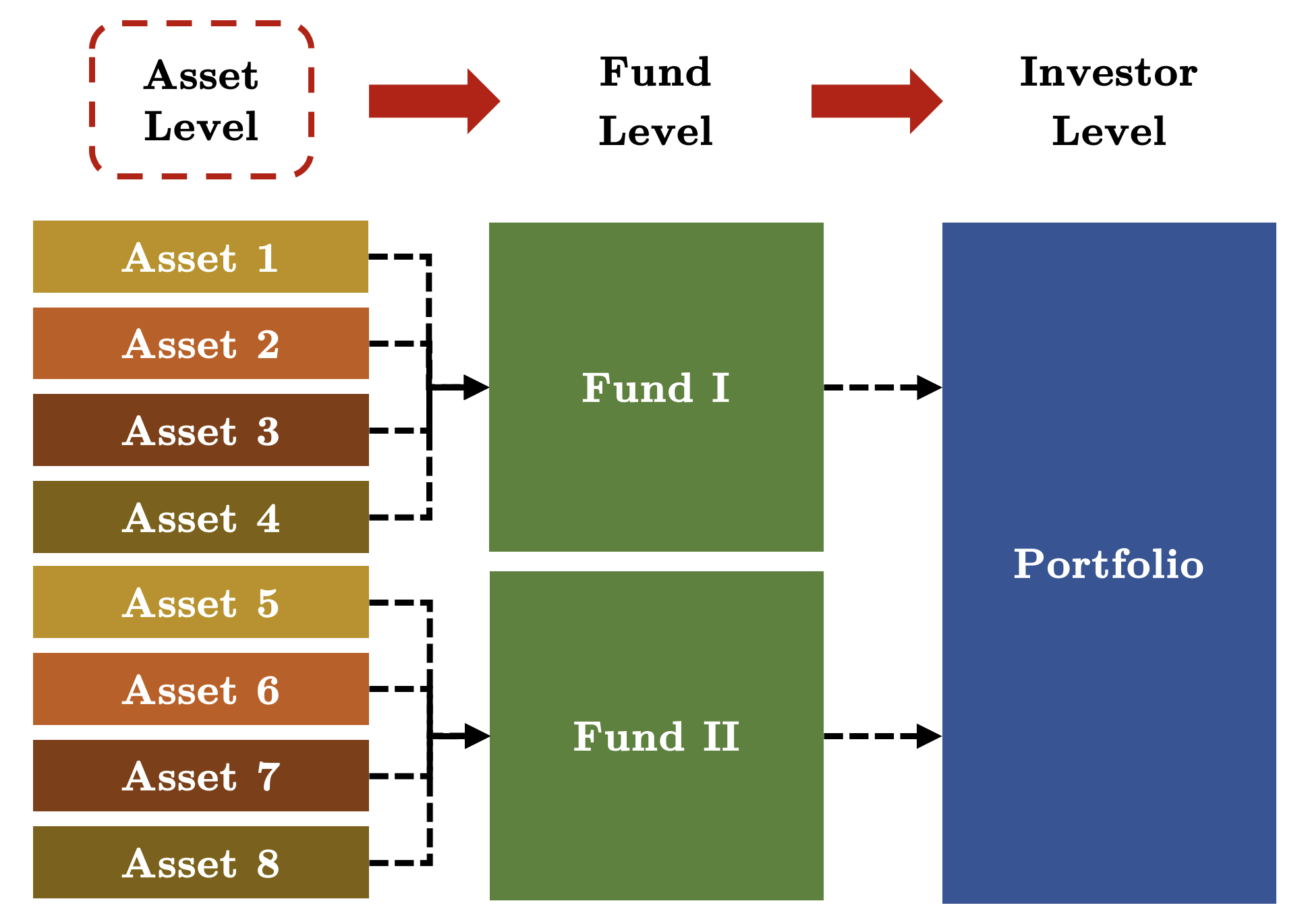

Asset level climate or nature value at stake is the negative NPV impact of physical and transition climate or nature risks plus the positive NPV impact of climate or nature related opportunities for asset. A translation to the fund level would then follow using economic weights of all fund assets and their CVaS and NVaS, and subsequently to the manager level. Once hazards are classified consistently across assets, exposures become comparable across assets and funds. Governance improves because functions operate from a shared classification, and outputs become decision useful for pricing, portfolio steering, and risk appetite.

Figure 2: Implementation process in assessing climate and nature related risk from assets to portfolio level. Source: Authors’ own conceptual model

Integration in Practice: A Four Level Roadmap

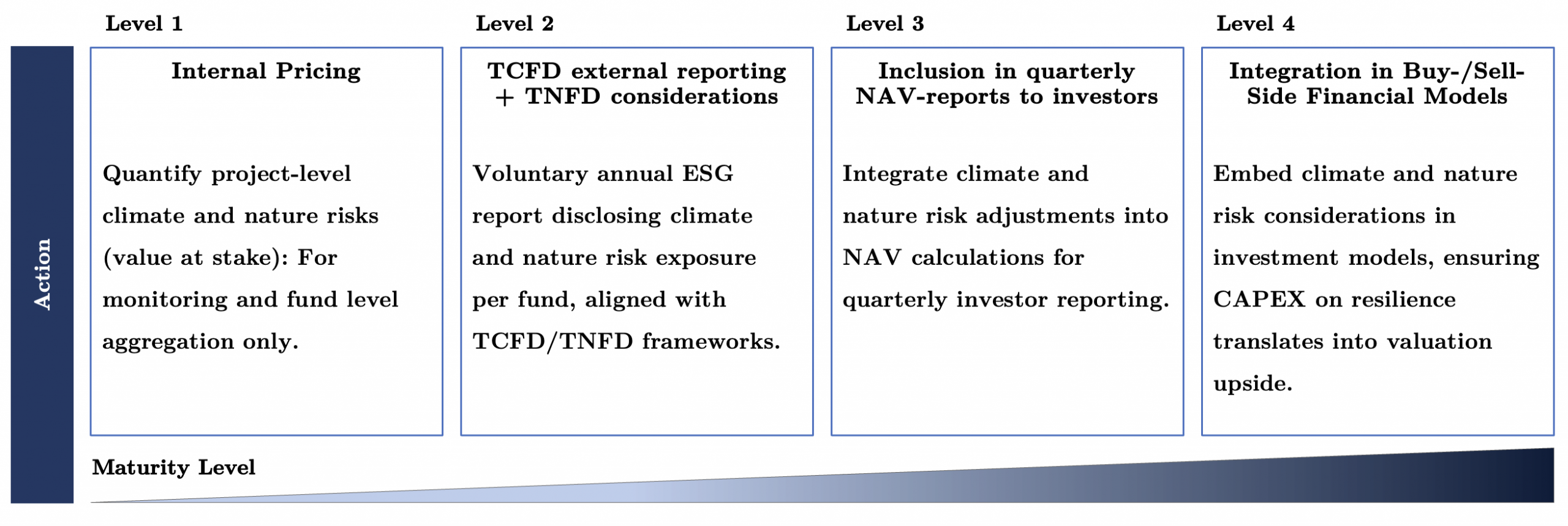

A taxonomy without integration into pricing, monitoring, and governance is little more than a concept. To close that gap, a four level integration pathway is proposed. Each level builds the capability required for the next, progressively embedding the management of climate and nature risk across the full organization.

Figure 3: Organisational maturity pathway for climate and nature risk integration. Source: Authors’ own conceptual model.

Level 1: Internal Pricing. At the first stage, managers quantify Climate Value at Stake (CVaS) and Nature Value at Stake (NVaS) at the asset level using the taxonomy. These adjustments remain internal and are not yet incorporated into reporting or investor communication. Even at this stage, they serve as a powerful internal risk valuation tool, establishing baseline exposure and supporting due diligence, monitoring, and mitigation strategies such as insurance.

Level 2: TCFD/TNFD Reporting. Once internal quantification becomes consistent and repeatable, transparency naturally follows. Climate risk disclosure aligned with TCFD signals analytical maturity to investors, and TNFD aligned nature disclosure is expected to follow as organizational capability deepens. While LP expectations for climate reporting remain more advanced, expectations on nature are accelerating rapidly. At Level 2, disclosure is not simply about voluntary compliance: it communicates to LPs that risks are systematically identified, structured, and governed. It reduces informational asymmetry between GP and LP, strengthens fundraising credibility, and responds to rising expectations for governance standards.

Level 3: Risk Adjusted Reporting. The third level marks a structural shift. Quantified risk adjustments enter quarterly reporting through a risk adjusted NAV presented alongside the base case valuation. A transparent bridge illustrates exactly how CVaS and NVaS affect fund level value. Internally, this elevates investment committee discussions by enabling portfolio comparisons that weigh resilience and risk concentration alongside expected return. Externally, it shifts LP conversations from qualitative assurances to structured valuation impact, establishing a common language between GPs and LPs around what is genuinely at stake.

Level 4: Full Financial Integration. The final stage is full integration from the outset. Climate and nature risks are embedded directly into base case assumptions during due diligence and underwriting: physical risks inform generation profiles, asset lifetimes, operating costs, and resilience CapEx, while transition risks shape regulatory assumptions, market outlooks, and discount rates. Opportunities are incorporated where credible and evidence supported. At this level, CVaS and NVaS are no longer separate analytical overlays. They are woven into acquisition pricing, portfolio construction, and exit strategies, and treated with the same rigor as market, credit, and liquidity risk.

A Fiduciary Imperative: This progression is fundamentally about fiduciary responsibility, not perfection. Climate and nature risk management does not require flawless models from day one. It requires active engagement with the risks, quantification of what can be quantified, transparent documentation of assumptions, and a commitment to refining them over time. Integration is iterative. But it must begin.

Implications for investors

Climate and nature risk management is rapidly becoming a gating criterion for capital allocation. Many managers already deploy quantitative tools to price and manage these risks. Those that remain reliant on qualitative narratives will fall behind, and the fundraising consequences will be real. Benchmarking is no longer limited to peers: leading LPs such as NBIM are building analytical capabilities that may soon price climate and nature risks more precisely than many GPs can internally. Managers that fail to keep pace with both peers and their most sophisticated LPs risk losing credibility and access to some of the world’s largest capital commitments. Sophisticated integration is not achieved overnight, and organizational complexity will inevitably slow adoption. A sequenced implementation approach is therefore proposed, with multiple viable paths to full integration. The direction, however, is unambiguous. LP expectations are rising, momentum is strong, and AI adoption across private market players and data vendors is accelerating the pace of geospatial risk assessment. Climate and nature risk management is a competitive advantage today. It will be a licence to operate tomorrow.

About the Authors

Daniel Schou is completing his MSc in Finance and Strategic Management at Copenhagen Business School, with a minor in ESG. Alongside his studies, he works in Responsible Investments at Velliv, leading sustainability due diligence across private equity, infrastructure, and private credit. His work spans GP engagement, benchmarking within private markets, and sustainability assessments of funds. Beyond due diligence, he develops LLM-enabled workflows for company risk assessments and contributes to SFDR data collection, analysis, and reporting. Daniel also serves as Head of Operations at CBS Investment Club, coordinating partnerships and events with firms in the financial sector. What drives him is building the tools and analysis that make sustainability data actionable for investment decisions, and integrating AI into that toolkit.

Nelly Chi is completing her Master in Management at ESSEC Business School and recently completed the Minor in ESG during her exchange semester at Copenhagen Business School. Alongside her studies, she gained experience in Singapore within a private equity fund focused on renewable energy investments in Southeast Asia, supporting financial modelling, investment research, and portfolio monitoring. She also contributed to sustainable finance initiatives within a French banking group, assisting with a Green Bond Allocation Report, developing an Excel-based tool to assess regulatory impacts on investment portfolios, and supporting work on an internal ESG impact framework. She hopes to contribute to investment strategies that combine financial discipline with meaningful environmental and social considerations.

Sebastian Manfred Streyffert is completing his MSc in Finance and Strategic Management at Copenhagen Business School, with a minor in ESG. Alongside his studies, he founded and runs Manfred & Co., an import company specializing in biodynamic and organic German wines, working directly with producers on sustainable sourcing and long-term market development. His thesis research focuses on how SMEs are indirectly affected by ESG regulation through value chain pressures from larger firms. Additionally, he serves as head of events at CBS Investment Club. Motivated by bridging compliance and strategy, he aims to institutionalize ESG practices in smaller companies to unlock competitiveness, operational efficiency, and long-term value creation in evolving European regulatory environments.

Christian Munch Jørgensen is completing his MSc in Finance and Strategic Management at Copenhagen Business School, with a minor in ESG. His master’s thesis investigates how sustainability-related incentives and ESG schemes are integrated into executive pay under the CSRD/ESRS regulatory framework across European countries and industries. Alongside his studies, he works at Cerius-Radius in Strategic Portfolio Management, supporting economic governance of investment projects across the electricity distribution grid by tracking budget changes, analyzing deviations, and consolidating asset and investment data. He also translates portfolio and budget data into decision-ready insights for senior management. Christian is driven by enabling the green transition through infrastructure and responsible investments that support a sustainable future.

Prof. Kristjan Jespersen is an Associate Professor in Sustainable Innovation and Entrepreneurship at the Copenhagen Business School (CBS). Kristjan is an Associate Professor at the Copenhagen Business School (CBS). As a primary area of focus, he studies the growing development and management of Ecosystem Services in developing countries. Within the field, Kristjan focuses his attention on the institutional legitimacy of such initiatives and the overall compensation tools used to ensure compliance. He has a background in International Relations and Economics.