By Lieto Cuccurullo, Eros Uber and Prof. Kristjan Jespersen

Every crash is an audit. When prices climb, almost any story about why a company is sound can pass for insight, because almost everything climbs together and nobody bothers to check the reasoning. Then the market falls, and the checking starts. The tide goes out, to borrow the old line, and you find out which beliefs were carrying weight. The pandemic crash tested one belief in particular. A great deal of capital still rests on it, so it is worth getting right.

The belief is simple enough. Companies with strong ESG ratings, especially the ones the major agencies all agree about, should hold up better when the world turns dark. It is an attractive idea. It is not even a foolish one. Five independent providers landing on the same view of a firm feels like proof that something real sits underneath, a business that is well run and not merely well marketed. And if that is true, these are exactly the companies you would want to own when the trouble starts.

Here is where it breaks. Look at how stocks moved through the crisis, set aside the ordinary market risk that drags every share around, and the ESG score explains nothing. The agreement between raters explains nothing either. This is not a matter of an unkind test. The resilience was never as solid as the consensus assumed; it only looked solid while the weather was calm. That ought to bother anyone who has been paying for it. A belief that survives only in good times is not really a belief. It is a habit.

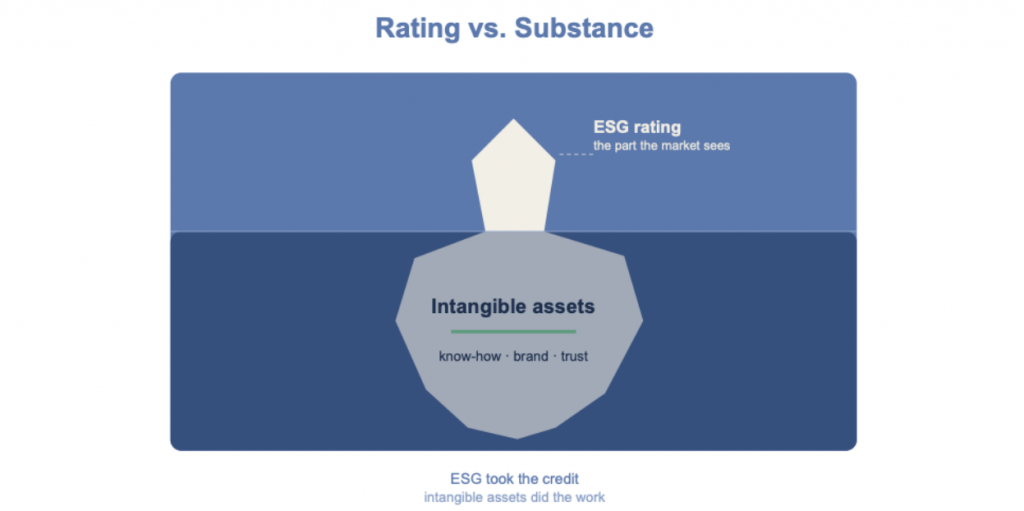

Something did carry firms through the shock. It just was not the rating. It was the depth of a company’s intangible assets, the know how, the brand, the trust built up with the people the business depends on. And here is the part worth sitting with: those are the very things a serious ESG programme tends to build. So ESG was not wrong. It was redundant. It kept claiming credit for a strength that belonged to plain company quality, while that strength quietly did the work. Label and substance had ridden together so long that the market stopped telling them apart.

Figure 1. Rating vs. Substance. ESG took the credit; intangible assets did the work.

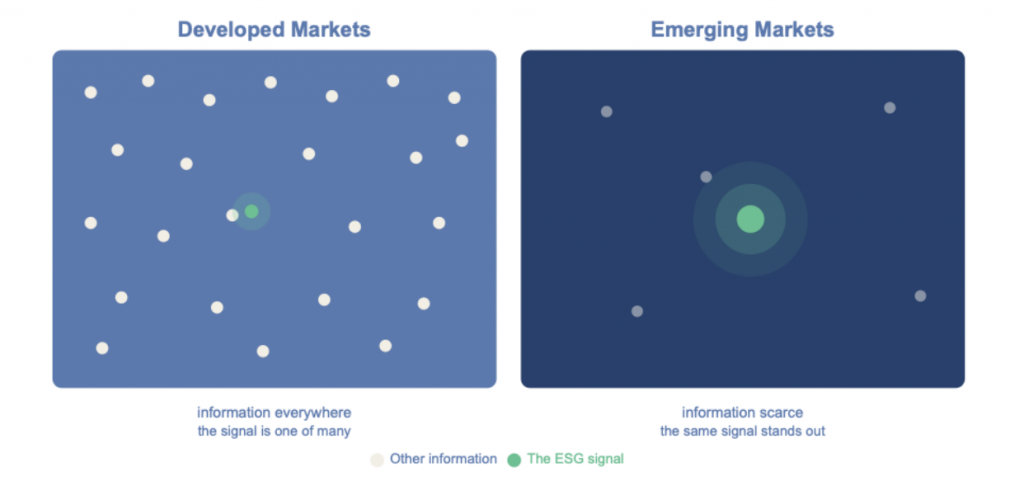

None of this means you throw ESG out, and the evidence is careful to say so. Two things held up. Where the signal did anything at all, it surfaced in the recovery and not the crash, once markets had the room to price the quieter details. Consensus also carried more weight in emerging markets, where investors have fewer other places to look. Hold on to that second one. It states the whole principle in a line. A signal is worth most where information is thin and least where it is everywhere. The same rating does not carry the same weight in Jakarta as it does in Frankfurt.

Figure 2. Developed Markets vs. Emerging Markets. Left: information everywhere, the signal is one of many. Right: information scarce, the same signal stands out.

So, no, ESG is not empty. But its usefulness is conditional, and most of the resilience people credit to it really belongs to the capability sitting underneath. For anyone putting money to work, that distinction is the entire game. Pay for the substance, the operational strength a company has truly built, and treat the rating as a clue to it rather than a substitute for it. The crash did not prove that sustainability fails to matter. It proved something narrower and more useful. It told us to stop mistaking the signal for the thing it is supposed to point at, and to ask, before leaning on it, which of the two we are actually holding: the signal, or the noise.

The Authors

Lieto Cuccurullo studied at Copenhagen Business School a MSc in Finance and Strategic Management and completed a minor in ESG and Sustainable Investments. Together with Eros he wrote a thesis on ESG ratings, provider agreement and stock price behaviour during the Covid-19 crisis. He currently works in the Commercial Strategy department at Trackman.

Eros Uber studied at Copenhagen Business School an MSc in Finance and Strategic Management, with an exchange semester at the University of St. Gallen. Together with Lieto he wrote a thesis on ESG ratings, provider agreement and stock price behaviour during the Covid-19 crisis. He currently works in the Global Strategy department at Circle K.

Prof. Kristjan Jespersen is an Associate Professor in Sustainable Innovation and Entrepreneurship at Copenhagen Business School (CBS) and Director of the Nordic ESG Lab. His research focuses on ESG indicators, sustainable finance, and the integration of environmental and climate-related risks into investment decision-making.