By Prof. Kristjan Jespersen, Alice Almgren and Tove Sellert Pehrsson

The EU Taxonomy, introduced in 2020 as part of the EU’s Sustainable Finance Strategy and the European Green Deal, is a landmark classification system designed to direct investments toward sustainable economic activities. Its primary objective is to boost market transparency and direct financial flows to activities that contribute to climate neutrality by 2050 (European Commission, 2024; European Commission, n.d.). However, translating these ambitions into actionable results has proven complex. From inconsistent data to challenging reporting requirements, both financial institutions and corporations face significant hurdles. This article explores the key challenges and opportunities associated with the EU taxonomy and its impact on financial markets, particularly Article 9 funds.

Our insights combine a review of academic and industry literature with a data-driven analysis.

Drawing on information from peer-reviewed journals and reports, we incorporate data from LSEG Workspace, including both directly reported and modeled estimates of EU Taxonomy alignment. Our analysis spans both company- and fund-level perspectives, covering all publicly listed European firms and Article 9 mutual funds, with data collected between October and November 2024.

Implementation Challenges and Data Gaps

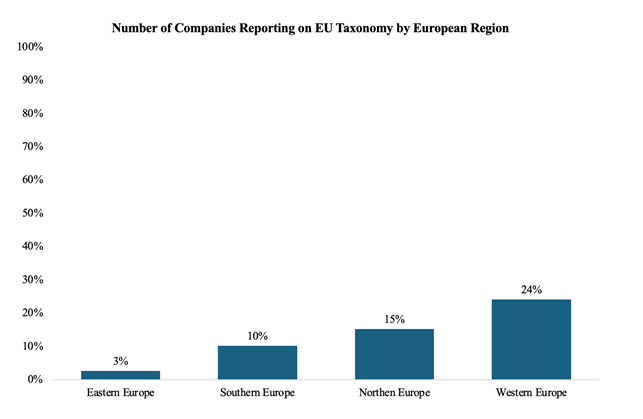

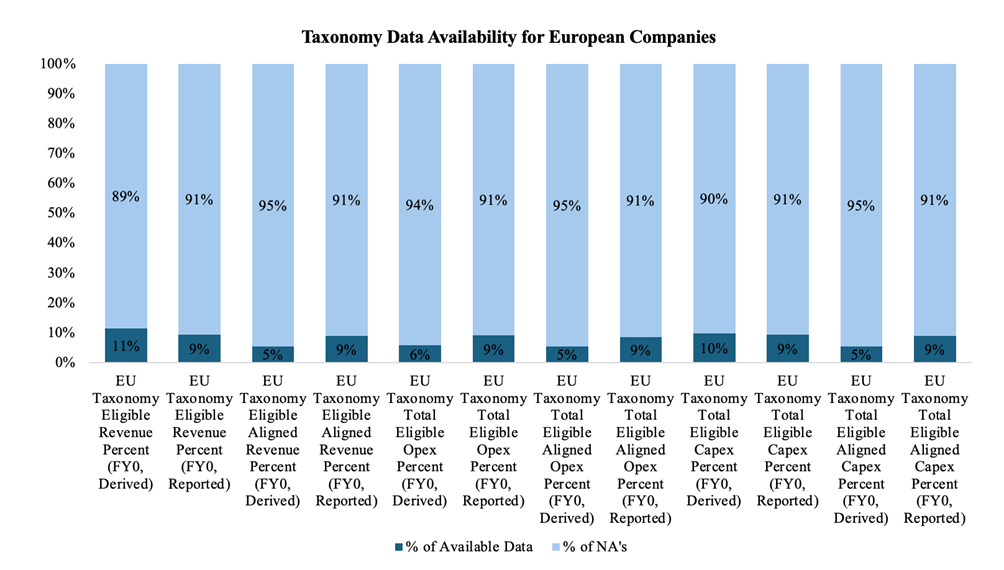

A key challenge in implementing the EU Taxonomy lies in its complex reporting framework. Companies and financial institutions must assess and disclose the extent to which their activities are eligible and align with the taxonomy’s environmental objectives. Eligibility serves as a foundation for companies to evaluate their activities against the taxonomy and determine whether they fit within its scope. Furthermore, to be considered aligned, activities must contribute substantially to at least one of the six environmental goals outlined in the taxonomy, while also meeting the Do No Significant Harm (DNSH) and Minimum Social Safeguards (MSS) criteria. However, organizations often struggle with understanding these requirements, leading to inconsistencies in reporting (Niewold, 2024; Hofstetter & Babayéguidian, 2024; KPMG International, 2024). Another major hurdle is data availability. Our analysis shows that only a small fraction of European public-listed companies report data relevant to the taxonomy, with coverage varying from 3% to 24% across different regions. Furthermore, missing data on key indicators, such as taxonomy-aligned revenue, capital expenditures (CapEx), and operating expenditures (OpEx) ranges from 89% to 95%.

These figures highlight the significant gaps that hinder comprehensive assessments of companies’ sustainability performances.

Figure 1: Number of companies (%) that are actively reporting on the EU Taxonomy by European Region

Figure 2: Data coverage for several EU Taxonomy metrics of public-listed European companies

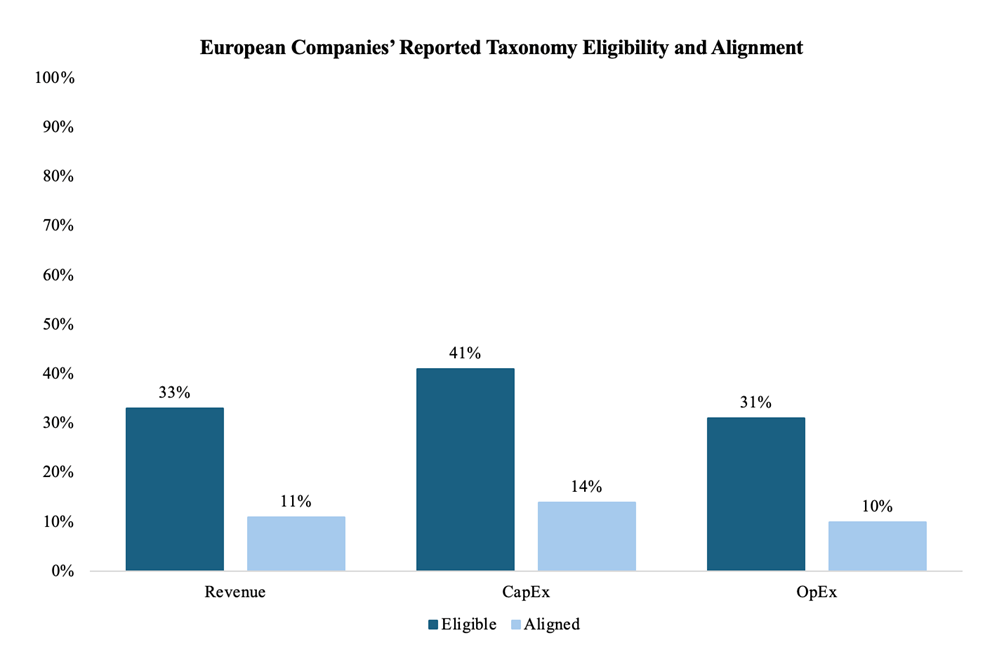

The discrepancy between the share of eligibility and alignment shows that while companies have been able to identify activities within the taxonomy’s scope, alignment levels remain substantially lower with public listed companies in Europe reporting 11%, 14%, and 10% aligned revenue, CapEx, and OpEx, respectively. These figures underscore the difficulties of achieving alignment, even as companies increasingly engage with the taxonomy’s scope and reporting requirements.

Figure 3: Average eligible and aligned revenue, CapEx and OpEx reported by public-listed European companies

Financial Institutions and Article 9 Funds Financial institutions’ occupy a dual role within the EU Taxomomy framework – they are both users and preparers of sustainable disclosures. This dual role makes financial institutions face additional complexity as their own disclosures are dependent on receiving information by other organisations (Garcia-Torea et al., 2024). Current gaps in data availability present challenges for financial institutions in implementing the EU taxonomy in their reporting and investment decisions. Detailed data on specific investments and companies is missing, making it difficult to clearly identify green investments under the taxonomy. There are also large discrepancies in how firms report alignment indicating challenges in implementation and reporting of the taxonomy’s criteria. This makes it difficult to trace financial flows to their direct impacts and to gain a clear overview of how finance connects to real sustainable activities. As a result, proxy indicators and simplified assumptions may be used, not covering the full picture of sustainable investments (Becker et al., 2024). This suggest that financial institutions not only face obstacles in gathering enough data to make informed investment decision but also in obtaining adequate information required for reporting.

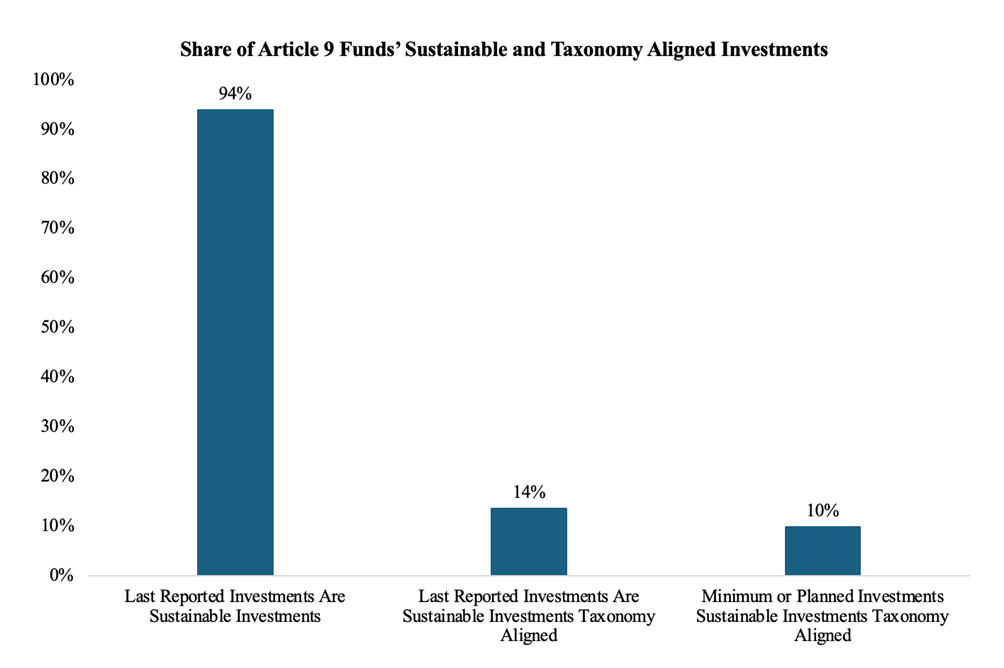

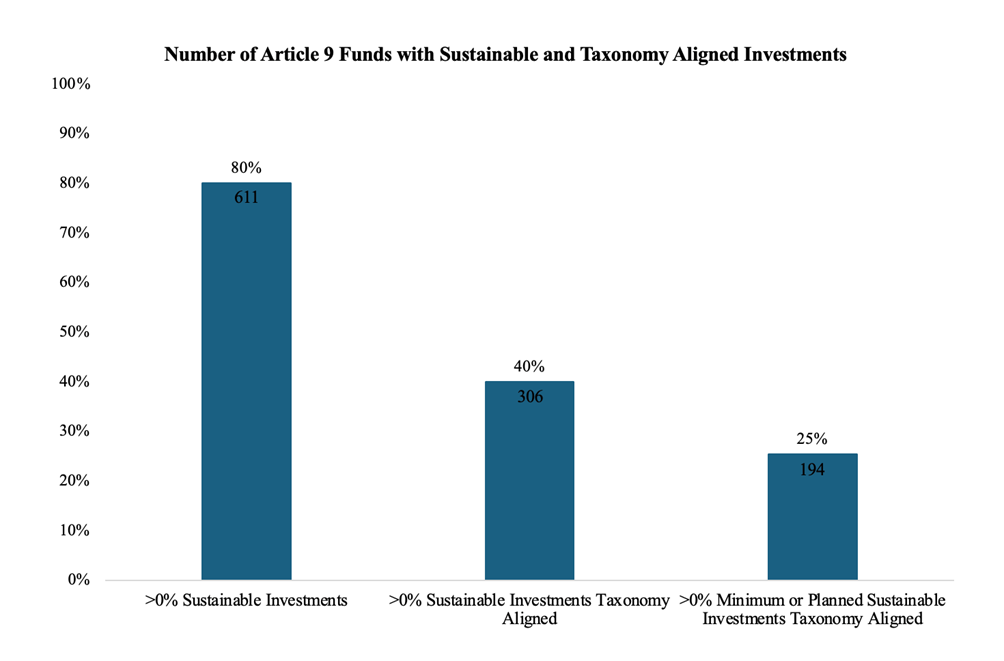

The situation is especially pronounced among Article 9 funds, which are classified under the SFDR as “dark green” and are expected to focus on sustainable investments. In our sample, while 80% of Article 9 funds report having sustainable investments, only 40% report any taxonomy alignment. On average, these funds report 14% of their portfolios as taxonomy-aligned, compared to a 94% share labeled as sustainable. These figures point to the practical limitations of taxonomy-based reporting in its current form, suggesting that the taxonomy may not yet offer a reliable benchmark for sustainability.

Furthermore, only 25% of Article 9 funds have disclosed in their Pre-Contractual Reports their planned or minimum share of taxonomy-aligned investments. The average share of such aligned investments is 10% among these funds. This means that even within the 25% of funds setting a commitment the average share of investments is small. This may be due to funds’ reluctance in committing to thresholds that they might not be able to meet, considering the findings that few funds have investments aligned with the taxonomy and those that do typically have quite small portions of their portfolios in these activities.

Figure 4: Number of Article 9 funds reporting on sustainable, taxonomy-aligned and minimum or planned taxonomy-aligned investments

Figure 5: Article 9 funds’ share of sustainable, taxonomy-aligned and minimum or planned taxonomy-aligned investments

Conclusion: Overcoming Complexity for Effective Implementation

The EU Taxonomy is a powerful tool with the potential to reshape how capital is directed toward sustainable activities. However, its current complexity and data gaps limit its effectiveness. For the taxonomy to fulfill its promise, stakeholders must prioritize streamlining reporting requirements, improving data availability, and setting more realistic expectations for implementation timelines.

Recent policy developments, such as the EU’s omnibus proposal, suggest that reforms are already in motion. Whether these changes will be enough to bridge the gap between intention and impact remains to be seen. As sustainable finance continues to evolve, striking the right balance between ambition and practicality will be essential for meaningful progress.

About the Authors:

Prof. Kristjan Jespersen is an Associate Professor in Sustainable Innovation and Entrepreneurship at the Copenhagen Business School (CBS). Kristjan is an Associate Professor at the Copenhagen Business School (CBS). As a primary area of focus, he studies the growing development and management of Ecosystem Services in developing countries. Within the field, Kristjan focuses his attention on the institutional legitimacy of such initiatives and the overall compensation tools used to ensure compliance. He has a background in International Relations and Economics.

Alice Almgren and Tove Sellert Pehrsson are completing their Master’s degree in International Business and Politics at Copenhagen Business School (CBS), with a minor in ESG and Sustainable Investments, where this project with London Stock Exchange Group was developed by their team under the guidance of Professor Kristjan Jespersen. Alice works in GN Store Nord’s Strategy and Transformation team, where she supports strategic and commercial projects, including go-to-market plans, channel strategies, and transformation initiatives. Tove works with strategic sustainability consulting at Ramboll Management Consulting, where she supports projects related to ESG strategy, corporate sustainability reporting, and responsible business conduct.

Passionate about sustainability and sustainable finance, Alice and Tove are currently writing their master thesis on the interplay between SFDR and the EU taxonomy and its impact on the reporting and investment decisions of Article 9 funds. Using fund data from LSEG Workspace and interviews with fund managers, their research examines the differences between Article 9 funds that report taxonomy-aligned investments and those that do not. It explores the broader implications of these reporting decisions on ESG-related behaviors and investigates why fund managers may choose to not report on the taxonomy. The goal of the research is to provide insights into how the relationship between SFDR and the EU taxonomy affect the credibility of sustainable investments.